Will AI kill buy-side junior roles? A bull/bear debate

It's your first day on the buy-side, you get your Bloomberg and sell-side equity research portal logins, sit through compliance training, and then a PM walks by your desk.

"My buddy who runs a fund mentioned this conglomerate stock. Seems interesting. Take a look and let me know what you think."

So you do. You pull 10-Ks, earnings transcripts, proxy statements, analyst day slides. You open Excel and start spreading the P&L numbers, bridging them to free cash flow, reading every supplemental KPI document to understand what actually drives the revenue and costs of this business.

Two or three days later, you walk through the sum-of-the-part thesis to your PM: the growth segments are undervalued, there's a real setup here. Your PM gets intrigued. You schedule an IR call in hopes of getting through to the CFO.

That 2-3 day process was your value-add as a first-time buy-side junior for the first year and a half on the job.

Then came the LLMs. Now that 2-3 day cursory work can be done in one hour.

What does that mean for the future generation of buy-side aspirants? I don't know the exact answer, but I have been reading Twitter comments of my phantom mentors whose opinions I respect.

The industry is at a fork in the road. The takeaway is that it is looking great for some of you while it looks bleak for others.

Here's the bull and the bear - just like you'd frame it for a stock.

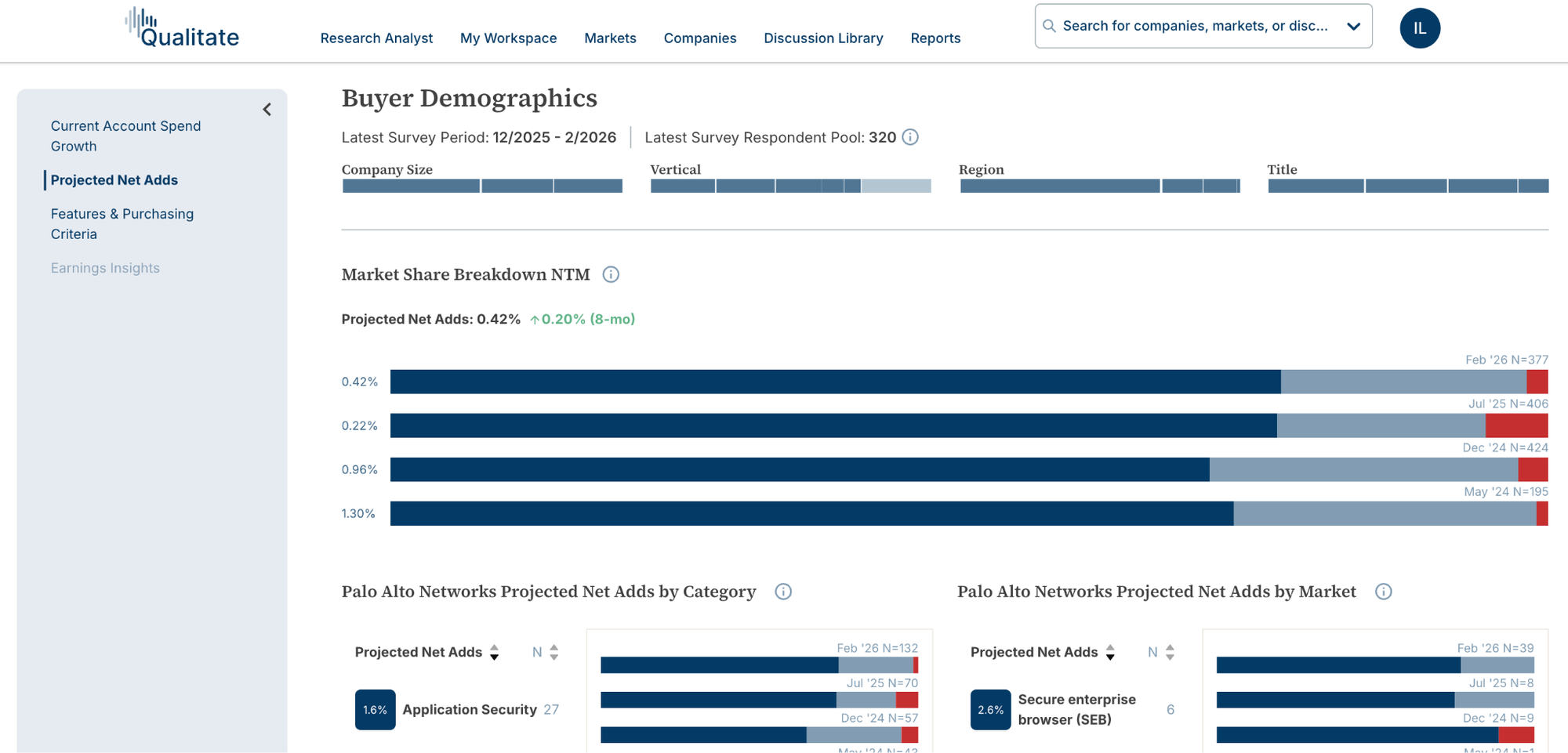

This week’s article is sponsored by Qualitate

Filings and earnings calls tell you what already happened. Qualitate captures what senior technology buyers are planning to do next.

Real-time purchasing intentions, competitive shifts, and adoption signals across 10,000+ companies, structured so you can track it over time.

Trusted by leading hedge funds and long-onlys.

The Bear Case: structurally less junior jobs

Funds have always hired from investment banking, private equity, and sell-side research for one primary reason: they didn't want to train anyone on the mechanical aspects of the job. They wanted people who could hit the ground running - people who already knew how to go from "take a look at this" to "Did the work. I think we should long / short / pass on this stock."

The mechanical work - the modeling, the transcript combing, the KPI build, the valuation - was the barrier to entry. And the barrier was high enough – that’s why many of you are still on the outside as you read this article. It was the reason junior seats existed. Firms needed headcount to turn over rocks (stocks).

Today, according to online chatters from respected investors, AI is good enough to remove that constraint entirely.

Now a senior PM can manage an army of agents running 24/7, producing the same quality of work a junior once took days to deliver. Idea velocity - which was always capped by how many humans you had doing the grunt work - is no longer a bottleneck.

What's left? Pattern recognition. Judgment. Position sizing. Portfolio risk management. The stuff that only a senior investor can do.

And here's the brutal logic that follows: if only a small percentage of people in this industry are truly alpha-generating investors by power law, those people just became more valuable than ever. Their bargaining power goes up. They can demand more pay - more importantly, more economics of the firm - because the firm's entire edge is now concentrated in fewer humans.

And if you are an aspirant who knows what you are doing, you will make more money than during the pre-LLM era.

Paradoxically, doesn't the promise of more $$$ attract more aspirants while knowing there will be less junior seats?

One challenge to this bear case: how do funds think about talent pipeline and succession planning? Maybe they just don't, because the assumption is the shift toward multi-managers will continue. Multi-managers - also known as "pod shops" - have always operated under a hire-fast, fire-fast model with no real succession planning. If a new pod is launched within the multi-manager, the business development team will go find new juniors. As long as juniors can follow the instructions on how to use AI to do the jobs the particular PM wants, junior turnover is not a concern.

The other concern is retention of star senior analysts. How do founders hedge the risk of losing their best people to a competitor or their own new firm?

Some challenges aside, the motivation to reduce junior headcount isn't really about comp – junior pay isn’t a big part of the fund’s labor cost (versus the PM and senior analysts.) The real driver is the desire to reduce operational complexity and the despise for training, which loops back to why the profession has always required entrants to have done IB, PE or ER.

Not to mention many senior investors are not nearly as great at teaching as they are at investing. Fewer humans means fewer hiring mistakes, less training overhead, less drama. They just prefer to be making money 100% of the time.

The Bull Case: junior seats survive but evolve

Here's the counter-argument: fund founders face the constant threat that their best people will eventually go start their own firms or join a competing pod with a bigger check.

To hedge that, firms still need a junior pipeline - not for the analytical work, but as an options portfolio on future talent. You hire juniors and see who develops pattern recognition, who develops conviction, who develops temperament under pressure.

The mechanical skills were never the real filter anyway. They were just the easiest thing to test. Dan Sundheim shared on the Cheeky Pint podcast that he has hired analysts with strong analytical skills and work ethic (D1 Capital hires only from elite private equity), but over time the stock-picking intuition just wasn't there. Unfortunately, the real job has always been making money in stocks, not just doing great research. And thanks to AI, less time is needed to see who actually has that intuition.

In this scenario, the junior role transforms. You're not the person who builds the model from scratch. You're the person who builds the agent workflow, improves the prompting, manages the research infrastructure - and then uses the time you've saved to develop the actual stock judgment that matters, whether that means doing case studies on previous longs and shorts, or talking to people to understand industries deeply.

Onboarding also gets easier. One of the oldest problems on the buy-side is that juniors don't know how to translate "take a look at this" into a structured process. If a firm codifies the PM's idea buckets, investment philosophy, and step-by-step instructions on how to use AI to execute the analytical work, that knowledge transfer problem largely disappears - fast-tracking a junior to forming actionable stock views as soon as possible.

Where do I land?

The bearish scenario seems more likely. Fund managers are openly saying they have retracted job openings because of AI - clearly they think it's getting to the point of good enough as a junior doer.

Many senior investors are bad at training. They either don't know how to articulate their process or they don't want to. Now they have the option to give structured instructions to a machine that executes reliably without needing handholding. That's not a hard choice for them.

What This Means for Buy-Side Aspirants

The 18-month grace period - where a new junior was expected to be building their reps - has collapsed. You should be good with the analytical work without having a buy-side job.

A few implications / conjectures:

- Will investment banking and private equity candidates remain the default candidate pool? The IB and PE path was prized because of analytical skills. If "vibe-modeling" using LLMs closes that gap for candidates with strong sector expertise or stock-picking intuition, will funds rethink their candidate targeting? And if funds rethink, will recruiters follow?

- Great time to pursue the buy-side … if you are good. If you're someone who already has a good track record picking stocks without having a seat, the same tools available to experienced investors are now available to you. You can be running an institutional grade portfolio all by yourself.

- AI knowledge will be a differentiator. Being well-versed in using AI in your research process can be a differentiator in interviews today, but overall it might just be a baseline requirement. Buy-side job descriptions increasingly list "AI skills" as nice to have - you should learn these skills ASAP to stand out.

- Use AI to augment, not replace. Build the fundamentals. Learn how to read a 10-K, a proxy statement, a press release, an earnings transcript as if AI doesn't exist. Then use AI to streamline the parts you can trust it with. But understand clearly: if you dump a transcript into a model and the output is wrong, the PM blames you, not the AI. The hallucination is your hallucination.

- One last thing - and this is the part that doesn't change no matter what AI can do: If you're using only publicly available sources available to everyone, you probably don't have a differentiated angle on the name. The best investors find insights in obscure footnotes, in conversations with the right industry gurus, in pattern recognition built over years. That's not something you can prompt your way into. All that is to say: there is still opportunity to generate alpha in the public market.

The game isn't over. It's just different. Let me know what you think - this is just a thought exercise. It will be interesting to revisit this article as AI continues to evolve.

Thanks for reading. I will talk to you next time.

Want my insider takes?

8,000+ readers get my weekly insights on public equity research.